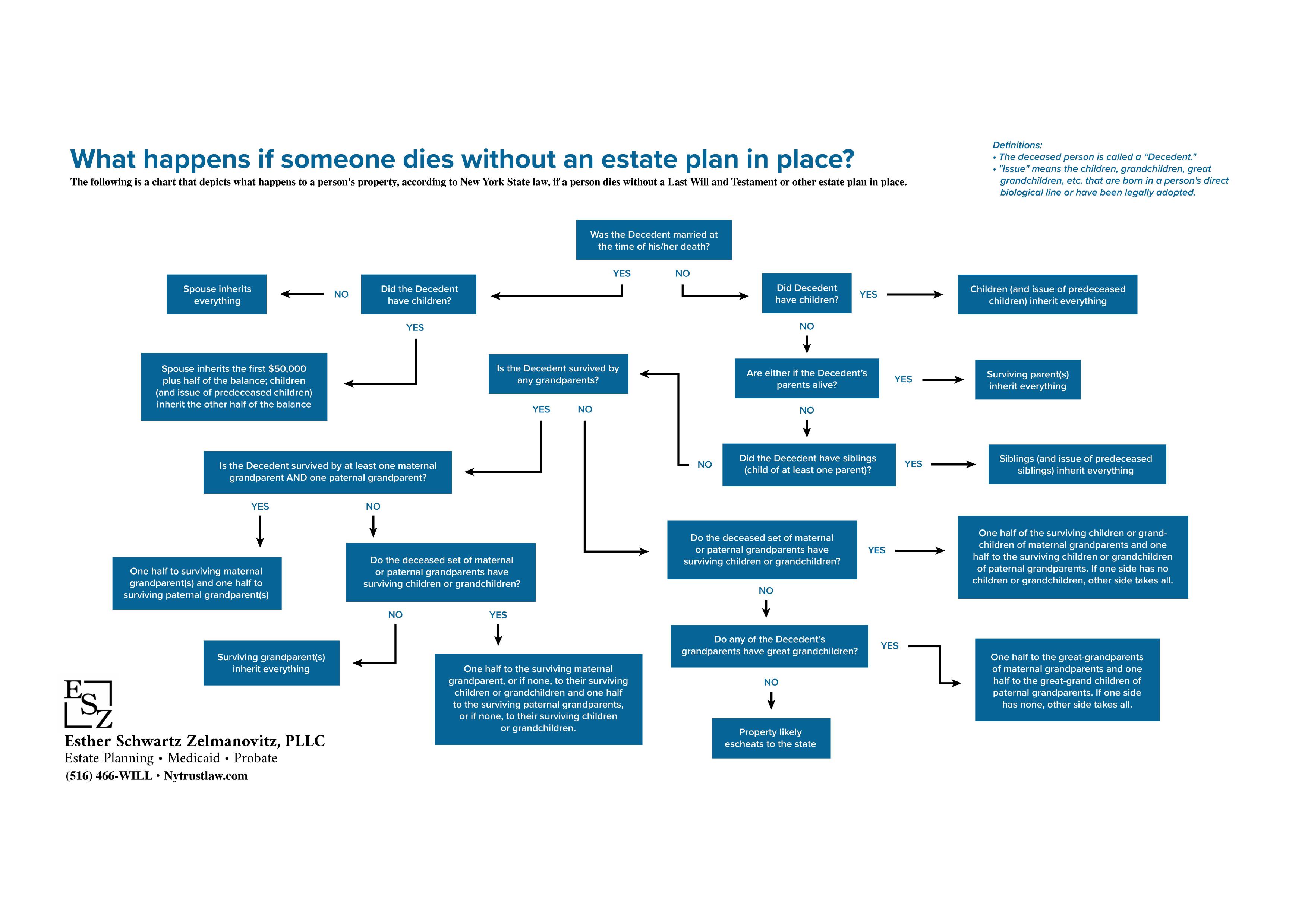

Long Island Trust Lawyer

A trust can be an important planning tool to manage your assets, as well as for passing your assets on to your loved ones. While trusts may offer exceptional benefits to those with substantial assets, a trust can be used in many different situations.

In fact, people may fail to appreciate the power a trust can have as a part of a well-crafted estate plan—a costly mistake. Trusts can be both flexible and powerful, containing instructions as to how and when to pass your assets on to your beneficiaries.

Many Long Island families see meaningful advantages when they create a trust as part of their overall estate strategy. New York law provides a variety of trust options to meet specific local needs, whether you are managing a second home in Suffolk County or minimizing estate taxes. Working with a trust attorney in Long Island brings valuable insight into state and local requirements, ensuring your trust reflects your unique family priorities and property goals.

Not only can a trust help keep your affairs private and allow your loved ones to avoid the probate of your estate, but a carefully crafted trust can also have the added benefit of minimizing or even eliminating estate taxes. A trust can preserve your assets in the event you need long term care and can also help you gain control over the distribution of your assets.

An effective trust is one that is carefully drafted by a qualified attorney who has a comprehensive knowledge of your specific situation, as well as a deep knowledge of current laws. After a thorough, thoughtful evaluation, an estate planning attorney from Esther Schwartz Zelmanovitz, PLLC can help determine if a trust is right for you, and, if so, which type of trust is most appropriate for you.

Rely on a skilled trust lawyer in Long Island. Contact us or call (516) 347-7356 now to arrange your consultation without delay.

Revocable Trust vs. Irrevocable Trust

Every trust is either a revocable trust or an irrevocable trust. As the names imply, a revocable trust can be changed or revoked entirely, while an irrevocable trust generally cannot.

While this is not an exhaustive list, both revocable and irrevocable trusts have the following benefits:

- Probate can be avoided, which means less cost, less time, increased privacy, and fewer court challenges or creditor claims.

- The estate and affairs remain private.

- You have greater flexibility and control over the distribution of assets.

- Provisions can address protection for disabled beneficiaries or those with financial challenges.

- Continuity of asset management continues if the grantor becomes disabled.

Families in Long Island often decide between revocable and irrevocable trusts by weighing their needs for lifetime control, tax minimization or elder law planning. Many Nassau and Suffolk County residents choose revocable trusts for flexibility, while others turn to irrevocable trusts for Medicaid planning and protecting assets from long-term care costs. A trust lawyer in Long Island can clarify which option fits your asset profile and state laws.

A revocable living trust allows the grantor to change the trust or withdraw assets at any time. The grantor can add property or remove it as needed.

Our Values, Your Peace of Mind The Principles That Define Our Firm

-

Compassionate, Relationship-Driven Service

We believe every client deserves to be treated with dignity, patience, and genuine care. Our firm fosters long-term relationships, guiding families with warmth and empathy through emotionally sensitive matters like elder care, estate planning, and loss.

-

Clear, Respectful Communication

We prioritize honest, prompt, and respectful communication. Whether answering questions or guiding you through complex decisions, we're responsive, dependable, and committed to making the process as smooth and stress-free as possible.

-

Serving with Integrity and Excellence

We hold ourselves to the highest standards of ethical practice and professional excellence. Clients can count on us not just for our legal knowledge, skill and experience, but for honesty, transparency, and unwavering advocacy on their behalf.

-

Tailored Legal Guidance for Every Client

No two clients are the same. We take the time to truly understand each client’s concerns, goals, and values, crafting customized legal solutions that reflect what matters most to them.

Living Trust vs. Testamentary Trust

Every trust is either a living trust or a testamentary trust. A living trust is a trust created during a grantor’s lifetime. A testamentary trust is a trust created under a person’s will, so is only created after death through the court probate process. There are advantages to setting up a living trust which can be managed and funded during your lifetime, without court intervention, and there are times when a testamentary trust is a more appropriate option. This would be determined based on each person’s specific objectives and needs.

Some specific types of trusts include:

- Medicaid Trusts help protect your assets from being spent down on long-term care. A Medicaid trust is an irrevocable trust that can help a person qualify for Medicaid to pay for long-term care such as nursing homes or home care. In New York, Medicaid has a five-year look-back period for nursing home care eligibility. You should fund a Medicaid Trust as early as possible, so five years pass before you need a nursing home.

- Irrevocable Life Insurance Trusts minimize estate taxes by removing a life insurance policy from your estate. These trusts provide legal and financial benefits, including keeping life insurance proceeds outside your taxable estate, offering asset protection for beneficiaries, and granting you more control over distributions compared with simply naming beneficiaries.

- Credit Shelter Trusts, Disclaimer Trusts, or Marital Exemption Trusts are created under a will or an existing trust to minimize estate taxes and remove assets from a surviving spouse’s estate. These irrevocable trusts use each spouse’s estate tax exemption to potentially reduce or eliminate federal or New York estate tax for a married couple. Your surviving spouse may access assets held in the trust, yet those assets do not become part of their taxable estate. When the surviving spouse passes away, trust assets transfer to the named beneficiaries.

- Special Needs Trusts (also called Supplemental Needs Trusts) are used to let a disabled person who receives government benefits such as Medicaid or SSI continue to use assets in the trust without losing those need-based benefits.

There are a number of other trusts to suit each specific need. While the above are general types of trusts, there is no trust that is a “one-size-fits-all.” Every trust has specific provisions tailored for each individual’s unique needs.

Understanding Common Mistakes with Trusts in New York

Many people in Long Island create a trust but overlook key steps or misunderstand New York's distinct rules. One common mistake is not re-titling local real estate or business interests in the trust’s name, which may cause those assets to pass through probate anyway. Others forget to update beneficiary designations on retirement accounts, leading to confusion or disputes among heirs. Some also misunderstand New York Medicaid eligibility rules and risk losing intended asset protection. Such issues add unnecessary delays and costs for families. When you plan ahead with a trust lawyer, you address these steps early and keep your intentions on track for your Long Island assets and loved ones.